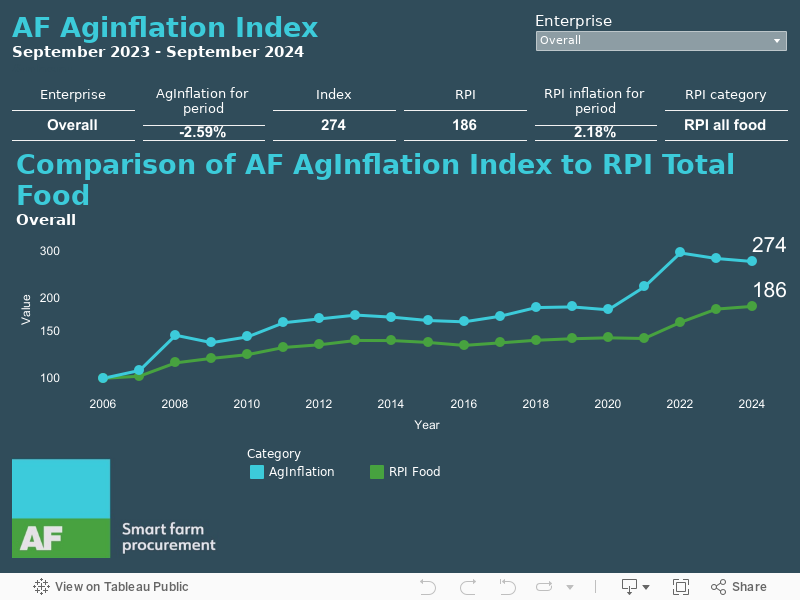

AF’s latest annual AgInflation Index reveals another welcome fall in overall cost of some farming inputs, but not all, in the year ended 30th September.

This average input cost reduction was -2.59%. But this is only part of the story.

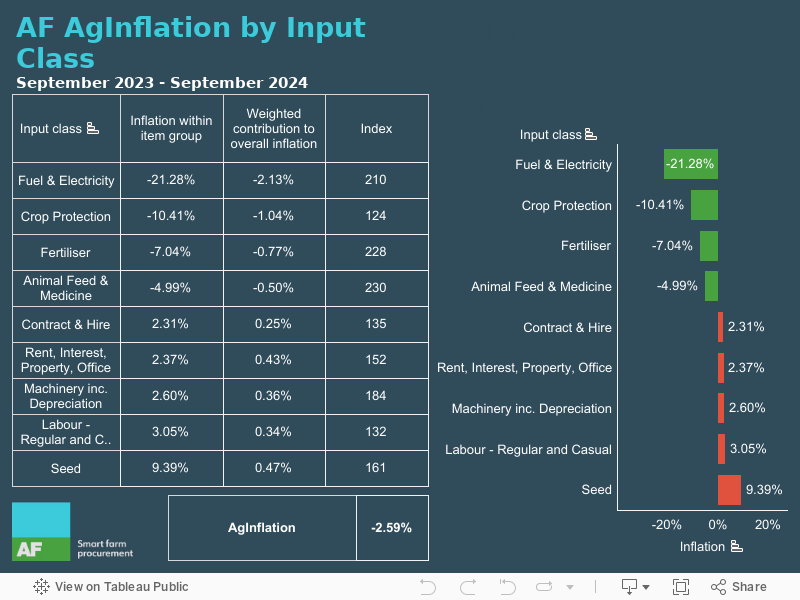

Five of the nine categories of inputs AF procures for Members have shown falling prices with fuel and electricity, crop protection products and fertiliser seeing greatest decreases at -21.28%, -10.41% and -7.04% respectively. However, the other four input categories showed increases with seed up by over 9% and labour, machinery and contract and hire all up by 2-3%. Meanwhile the Retail Price Index (RPI) held steady at 2.18%.

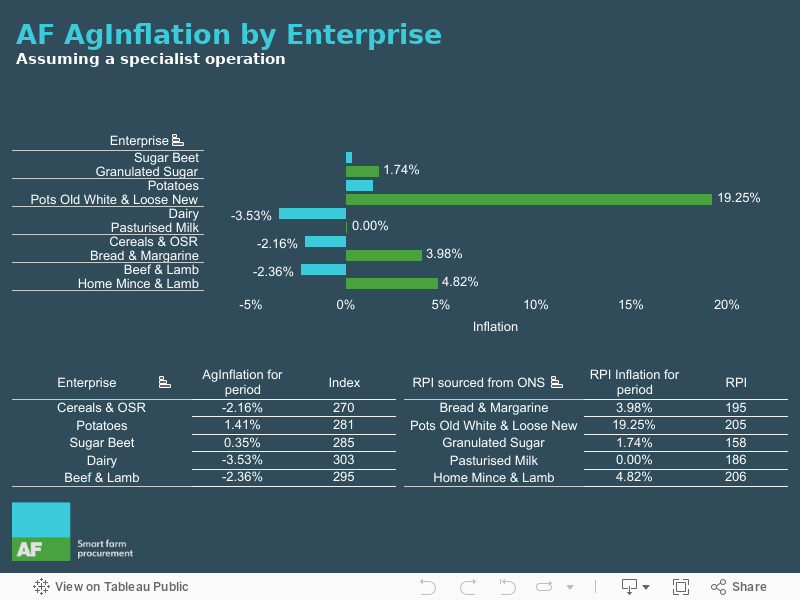

Cereals and OSR – Our latest AF AgInflation figures show a reduction in cost of growing cereals and OSR of -2.16%, and RPI for bread and margarine has increased by almost 4%. The reduction in variable costs will not alleviate financial threats to overall margins from tricky establishment conditions followed by lower average yields in harvest 2024.

Potatoes – costs to produce potatoes in the year to September 2024 increased by just under 1.5% compared to 2022/23, but the price paid for consumers over the last year went a good way to cover that as the cost to shoppers for stored potatoes and new in the last year increased by 19.25% according to the RPI, driven by lower volumes in store from difficult 2023 harvest. Adverse weather has made conditions difficult this year too.

Sugar beet – production costs have increased slightly in the year to September 2024 by just 0.35%, and the price of granulated sugar in the shops has increased again, but only by 1.74%. The total area UK sugar beet in the ground this year is the highest for over three years at just over 100,000 ha perhaps driven by optimism about year on year improving margins for this crop.

Dairy – the cost of dairy farming has followed the input prices downwards, helped significantly by drop in the cost of energy by -21.28% from record highs, and fall of -5% in feed and medicine costs to contribute to overall deflation in inputs measured at -3.53%. However, unlike the other four of the production sectors, milk prices paid by consumers show no increase in value in the RPI.

Beef and lamb – production costs have reduced in the year to September 2024 by -2.36%. The retail price of minced beef and lamb has increased by nearly 5% over the same period. During the same period government statistics revealed the falling total numbers of cattle and calves (-2%) and sheep and lambs (-4.3%).

The total food Retail Price Index (RPI) for a basket of foodstuffs has risen over the same one-year period by an average of just over 2%, a repeat of the previous two years’ trend.

The gap between farm input costs and retail prices continues to narrow. According to AF, the RPI is lying almost parallel with – but still significantly below – increased farm input costs. The interesting thing to look for in the AgInflation figure this time next year is whether these lines continue to converge.

AF Members and other rural businesses value the hindsight, especially for their negotiations for contracts, particularly in potato and fresh produce supply. But foresight is financially just as important and for this AF procurement specialists share their analysis of AF AgInflation October 2024.

Barry Crossan, AF Head of Utilities, explains “Electricity deflation is mainly due to reduction in overall demand supported by strong availability of product and favourable weather conditions.

Power generated from renewables (wind in particular) has been strong and consistent. Weather has been warmer.

There are good levels of gas storage across Europe which makes it easier to cope with peaks in demand for heat and electricity generation without price spikes. Wholesale prices have flattened over summer months at levels about £20/MWh below similar time last year.

Presently, the outlook for rest of 2024 seems settled this side of Christmas but major factor will be any weather developments going into 2025.”

On seed and crop protection products, AF Head of Crop Inputs Lee Oxborough adds “The key driver in seed price inflation was poor Autumn ‘23 conditions. This impacted availability and quality of seed crops, driving prices up in the Spring.

We saw the opposite in crop protection, where the poor conditions led to a smaller cropping area for applications. As a result we had a market place busy with product choices, resulting in prices falling. This put AF in a strong position in negotiation of your crop protection products, which you can see reflected in our AgInflation numbers.”

Helen Thurtle, AF Fuel Strategy Procurement Manager, adds “We are experiencing a two year price low, with diesel prices down by almost 25% (20 pence per litre).

Geopolitical events, such as conflict in the Middle East, continue to influence daily market swings and rumblings of supply cuts could affect the longer-term outlook.”

AF Chief Executive David Horton-Fawkes adds “Although the headline fall in AgInflation over the last year is encouraging, the devil is in the detail. Our Members are running their businesses on wafer-thin margins and there is a big impact in small differences.

We know our AgInflation index is used by Members to scrutinise their plans, and to negotiate with processors and retailers and it is good to continue to provide independent evidence to help them with that. It’s also good to see retail prices beginning to reflect the costs of production.

AF Members can rest reassured that our procurement teams are working on their behalf to protect their margins in 2025 and beyond so they can focus on producing food and other crops.”

© 2023 The AF Group Limited

Society Registration Number: 29539R. The AF Group Limited is a mutual company formed under the Co–Operative & Community Benefit Society Law.

Calls are recorded for training and monitoring purposes. Recordings are used for our own purposes only.

Image: Towfiqu Barbhuiya, Unsplash.com

Sitemap | Privacy | Terms and Conditions | Cookies | Website Design by Naked Marketing